Understanding tax return

Every year, you must declare your income to the tax authorities. This includes revenue from investment income, as well as any capital gains or capital losses on the disposal of your shares. We are here to help you fill out your tax return.

The elements of taxation in this page apply to French residents for tax purposes. More information for residents outside France in the section "Residents outside France"

Tax conditions for securities explained

The entirety of your income from financial investments is referred to as your “investment income.” As an Air Liquide Shareholder, this includes:

- dividend payments,

- any capital gains on the sale of your shares

- the payment of fractional rights during free share attributions.

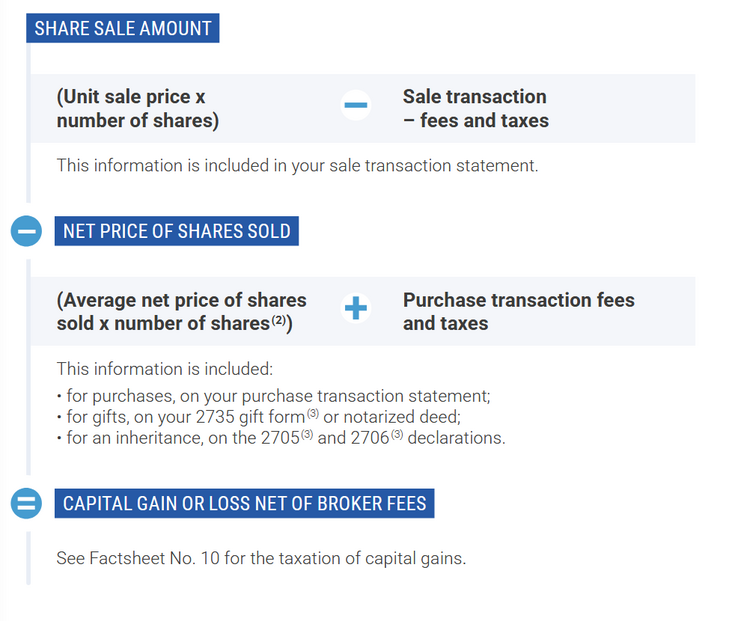

To fill out your 2026 tax return, refer to your 2025 tax reporting form as it contains all of your investment income information. Simply copy the stated amounts of dividends and fractional rights in the relevant boxes of your tax return. Any fractional rights received must be declared as a capital gain on sale, without applying the deduction (in box 3VG). Your tax reporting form also contains your gross disposal amount. The resulting capital gains must be declared.

If you are a direct registered Shareholder, access your Shareholder Portal to find your document.

Choosing the best taxation method

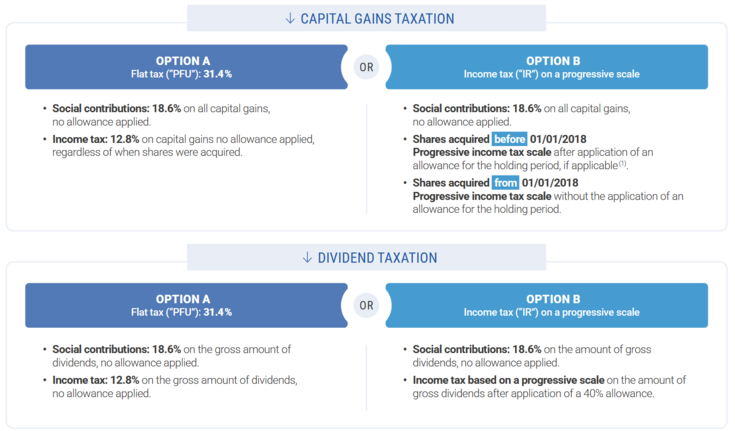

Every year you can choose between the 31.4% flat tax or the progressive scale. The option chosen will apply to the entire household’s investment income. We recommend using the tax authorities’ simulator on the impots.gouv.fr website (for french residents only). Please contact your local tax authorities if you have any questions.

How are capital gains on sales taxed?

(1) A 50% allowance is applied if shares are held for between two and eight years, and 65% if they are held for eight years or more.

Capital losses are deducted from capital gains before the seniority deduction. The seniority deduction is then applied to the resulting balance, thereby providing the taxable amount. This deduction is related to the seniority of the securities sold that resulted in a capital gain when using the progressive income tax rate and only for securities obtained prior to January 1, 2018.

You are responsible for calculating and declaring in Form 2042C the seniority deduction applied to your capital gains (box 3SG) and the amount prior to deduction of taxable capital gains (box 3VG) or losses (box 3VH). Form 2074 can help you itemize your calculations. Capital losses should first be deducted from capital gains of the same year, but it is possible to carry them forward for up to 10 years.

Taxing dividends

Tax on dividends received in 2026 is paid in two stages:

- In 2026, when dividends are paid in respect of the 2025 fiscal year:

- If you sent a request to your account manager for an exemption from advance withholding before November 30, 2025, only the social contributions of 18.6% will be withheld;

- If you did not send a request to your account manager to benefit from this exemption before November 30, 2025, social contributions of 18.6% will be withheld along with advance withholding of 12.8%, for total advance withholding of 31.4%.

We remind you that you are personally responsible for declaring your income and capital gains from the sale of securities to the tax authorities. The data made available to you is intended to facilitate your procedures and is provided for information purposes only, based solely on the elements available to Air Liquide. Air Liquide cannot, under any circumstances, be held responsible for the accuracy of the information you report in your tax return.

-

In 2027, when you pay any remaining income tax owing on your 2026 investment income: dividend taxation will only be withheld if you have requested an exemption from advance payments.

A new statutory rate equal to at least 12.8% is withheld upon dividend payment by your account manager. However, in most cases, a tax agreement2 is signed between France and your country of residence. The main aim of this agreement is to set a flat tax rate which is withheld from your dividends.

To benefit from this rate, you must send form 50003 (corresponding to the request to apply the rate adopted in the agreement), completed and signed by the tax authorities of your place of residence, to your account manager by mid-April. This form must be resent to your account manager each year. Otherwise, the statutory rate of 12.8% will be applied upon payment of the dividend.

3 Cerfa form n°12816*01-02